TL;DR

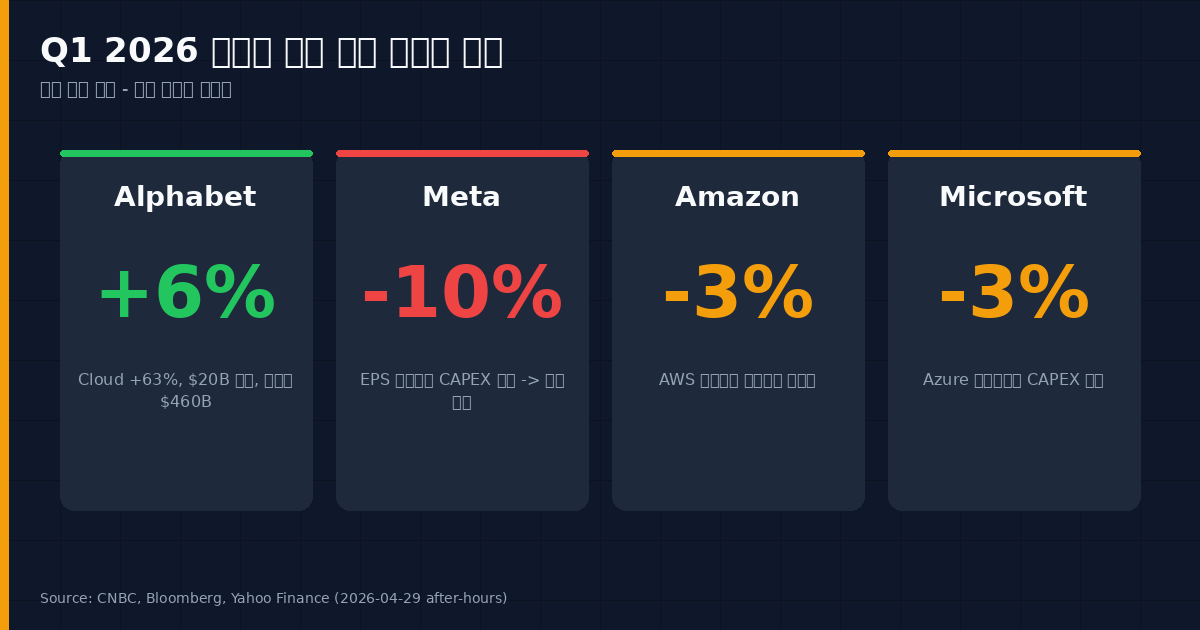

- The Beat Wasn’t Enough: All four hyperscalers beat consensus on revenue and EPS. Reactions ranged from +6% (GOOGL) to -10% (META).

- The New Rule: Markets stopped applauding AI capex. They started pricing AI revenue. Cloud monetization is now the swing variable.

- Positioning: Long GOOGL on Cloud throughput, underweight META until ad revenue reaccelerates, and watch Korean memory names for second-order capex absorption.

Same Beat, Opposite Tape — Read the Spread, Not the Headline

On April 29, four trillion-dollar companies reported within an 80-second window. Every one beat. Then the market voted.

| Ticker | After-Hours | Pivotal Variable |

|---|---|---|

| GOOGL | +6% | Cloud +63% YoY, $20B quarterly run-rate |

| META | -10% | 2026 capex raised to $125–145B |

| AMZN | -3% | AWS solid, guide conservative |

| MSFT | -3% | Azure strong, capex digestion |

The spread tells the story. For two years, the trade was simple: announce more AI capex, get a higher multiple. That trade is dead. The market is now asking a harder question — show me the revenue line tied to the spend. Alphabet showed it. Meta could not.

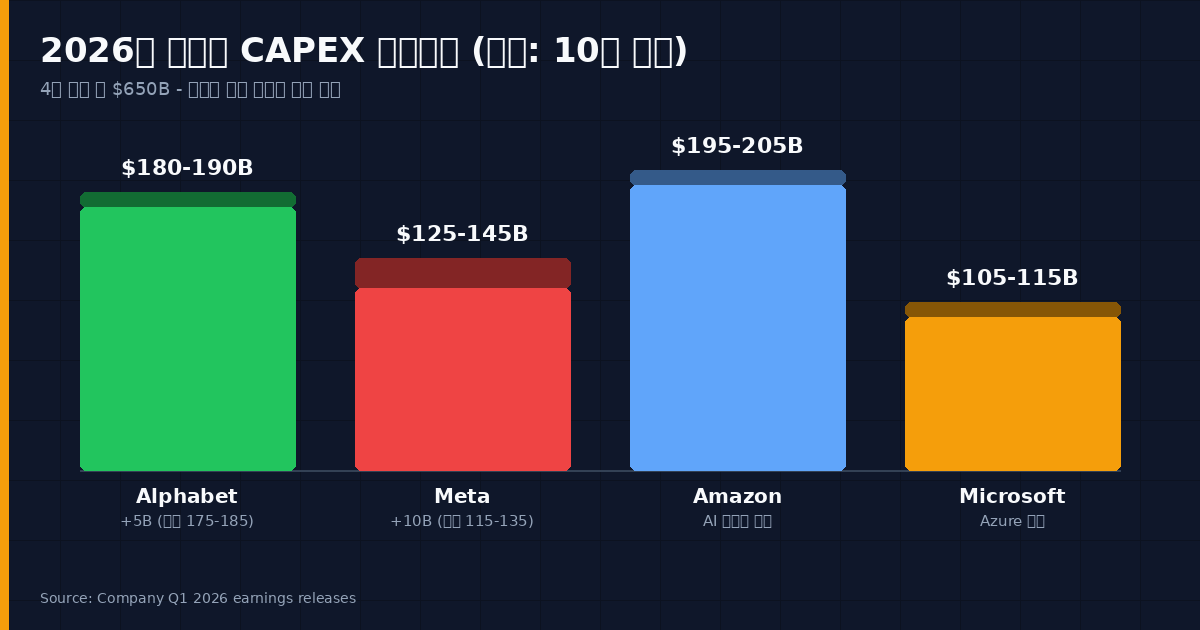

The $650B Question

Combined 2026 capex guidance from the four hyperscalers now points to roughly $650B. That’s the new baseline. The interesting detail is why the guides went up this quarter — Meta said it on the call: memory pricing.

Alphabet bumped the range from $175–185B to $180–190B. CFO Anat Ashkenazi told the call that 2027 capex will increase meaningfully versus 2026. The investment cycle is not slowing. The market just changed what it’s willing to pay for it.

Why Alphabet Got Paid

The +6% move on GOOGL is explained by three numbers, in order of weight.

1) Google Cloud at $20B, +63% YoY. Not just a beat — an acceleration. Cloud is the only revenue line in the hyperscaler universe with a clear, visible link to AI capex. Pichai’s exact framing on the call: “Enterprise AI solutions became the primary growth driver for Cloud for the first time in Q1.” That is the sentence that moved the stock.

2) Cloud backlog of $460B. Roughly 23x the quarterly Cloud run-rate. If you assume four-to-five-year recognition, this backlog underwrites the entire $190B 2026 capex envelope on signed contracts. That is the cleanest visibility metric in the megacap complex.

3) Total revenue $109.9B (vs $107.2B est), +20% YoY — Alphabet’s fastest growth quarter since 2022. The “AI cannibalizes Search ads” thesis from 2024 is, for now, wrong.

Why Meta Got Punished

Meta’s print was structurally fine. Revenue $56.31B vs $55.45B est. Adjusted EPS $7.31 vs $6.78. A high-single-digit beat. The stock dropped 10%.

Three things broke.

Capex range raised by $10B at the top end ($115–135B → $125–145B), with no matching new revenue line. The company cited memory pricing — meaning a chunk of the increase is input cost inflation, not new ambition. That is the worst kind of capex revision.

Q2 revenue guide of $58–61B implies flattish sequential growth. Ad pricing momentum is not accelerating into a $130B-plus capex year. The ratio is moving the wrong way.

No Cloud-equivalent. Reels monetization and the MTIA chip roadmap are the right answers — eventually. But Meta has no separately disclosed revenue line that tracks AI infrastructure spend the way Cloud does for GOOGL and AMZN. That is a structural disclosure gap, and the market priced it.

The cleanest framing: Alphabet became “the company earning from AI.” Meta stayed “the company spending on AI.” Same earnings beat, different multiple regime.

Competitive Context — Where Amazon and Microsoft Land

AMZN and MSFT both fell ~3% despite reasonable Cloud prints. AWS and Azure both grew at AI-accelerated rates, but neither company gave the kind of forward booking number Alphabet disclosed. In a market that just raised its bar on visibility, “in line with strong” reads as “not enough.” The MAG-7 is no longer a single basket trade.

My Verdict / Positioning

Long GOOGL. The Cloud monetization curve is real and the $460B backlog is the cheapest insurance policy in megacap. Multiple expansion is justified on the throughput, not on hope.

Underweight META until two things print together: a re-acceleration in ad pricing AND a separately disclosed AI-infrastructure-linked revenue line. The capex-to-revenue ratio is moving the wrong way and the market will not pay for that twice.

Neutral on AMZN and MSFT. AWS and Azure are good businesses with bad timing — they reported into a tape that suddenly demands disclosure both companies don’t currently provide. The fix is operational, not structural; it just takes another quarter or two.

Long Korean memory exposure (SK Hynix, Samsung) as a second-order trade. When Meta’s CFO explicitly cites memory pricing as a capex driver, that is a primary-source signal — not a sell-side estimate. Roughly $650B in combined hyperscaler capex routes a meaningful portion through HBM and DDR5. Korean memory leaders sit on the receiving end of a guidance raise the market just confirmed.

Three Signals to Watch Into Next Quarter

- Revenue growth versus capex growth, by company. Two consecutive quarters where capex growth outpaces revenue growth = multiple compression. GOOGL is in good shape. META is on the clock.

- Backlog/RPO disclosure. Whoever reports the next $400B+ backlog number gets the next leg of multiple expansion. Watch MSFT first.

- HBM pricing trajectory. The single variable that ties hyperscaler margins to Korean semiconductor earnings. The two will move in tighter correlation than at any point in the last decade.

Bottom Line

The era of “spend on AI, get rewarded” ended on April 29. The new era — prove AI revenue or get repriced — started the same evening. Alphabet is the template. Meta is the cautionary case. Position for the spread, not the headline.

Disclaimer: This is an analytical memo based on public filings and reporting (CNBC, Bloomberg, Yahoo Finance, company releases). It is not investment advice or a solicitation to buy or sell any security. All positioning views are the author’s own and may change without notice. Do your own diligence.