TL;DR

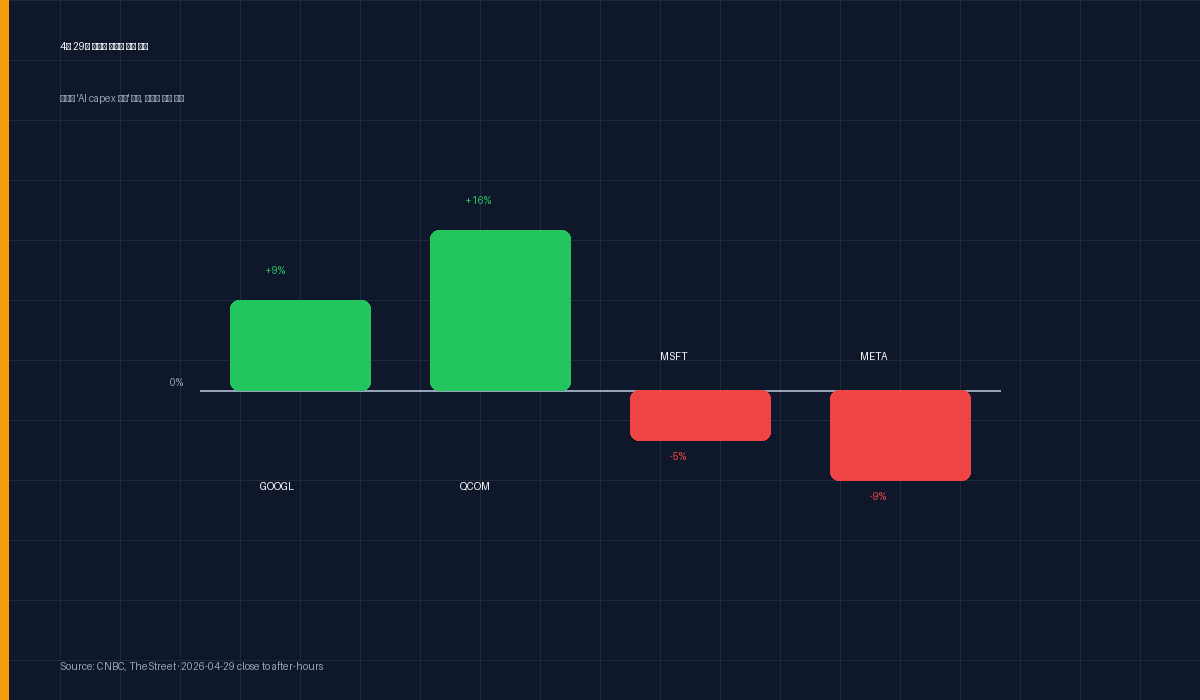

- The Split: GOOGL +9% on $180-190B capex guide. META -9% on $125-145B. MSFT -5%. Same headline, opposite reactions.

- The Rubric Shift: The market is no longer pricing capex announcements on size. It’s pricing them on revenue evidence.

- My Verdict: Overweight Alphabet and Korean memory (HBM); Watch on Meta until Q2 monetization data; Trim Microsoft on relative growth deceleration.

Same Capex Bump, Opposite Tape Reactions

After Wednesday’s close, four megacaps and one chipmaker delivered a stress test of the market’s AI thesis. The reactions were not subtle.

| Ticker | 2026 Capex Guide | After-Hours |

|---|---|---|

| GOOGL | $180B – $190B (raised) | +9% |

| QCOM | n/a (guide beat) | +16% |

| MSFT | Quarterly $35B+ run-rate | -5% |

| META | $125B – $145B (raised) | -9% |

Alphabet committed to spending $45-65 billion more than Meta in 2026 — and was rewarded for it. Meta committed less, and got crushed. The traditional “capex up = margin pressure = stock down” reflex didn’t fire for GOOGL. Understanding why is the entire trade.

The Number That Justified $190 Billion

Alphabet’s print included three figures that made the capex line read like a leading indicator instead of a cost line.

- Google Cloud revenue: $20.0B, +63% YoY. Fastest of the hyperscaler trio.

- Cloud operating income: $6.6B vs $2.2B prior year. Roughly 3x — margin expansion at scale.

- Cloud backlog: $460B+, nearly doubling sequentially. That is contracted, future-billable revenue already on the books.

The rest of the print supported the thesis: total revenue $109.9B (+22%), net income +81%. CFO Ashkenazi explicitly told the call that 2027 capex will rise materially above 2026.

The market is not pricing $190B as a bet. It’s pricing it as demand-pulled supply. Backlog leads capacity; capacity leads capex. When the order book is up almost 100% QoQ, datacenter spend is the second-derivative effect, not the first.

What the Market Saw in Meta That It Didn’t See in Google

Meta’s problem isn’t the dollar figure. It’s the monetization channel.

Alphabet has an external customer for the marginal compute it builds: Cloud customers. Spend more → sell more GPU-hours → recognize more revenue. The flywheel is observable.

Meta does not have an external compute buyer. The marginal datacenter feeds:

- Internal ad ranking and recommendation models

- Reels content matching

- AR/VR R&D

- Llama training

All of these are second-order monetization — the assumption is that better models lift ARPU on the existing ad business. That assumption may even be correct, but it’s a narrative bet rather than an evidence bet. With user growth decelerating and Zuckerberg signaling further capex acceleration into 2027, the implied payback period extended materially. The street repriced.

Microsoft (-5%) sits between the two. Azure is an external compute buyer like GCP, but its growth has plateaued at +26-27% for three straight quarters. Versus Google Cloud’s +63%, the relative momentum is a problem. The capex bill is similar; the evidence supporting it is weaker.

How the Grading Rubric Changed Wednesday

What changed Wednesday is the grading system, not the bias. Through 2024-2025, the market gave hyperscalers credit for capex on faith — AI was the future, and spending was a proxy for ambition. Wednesday, the market revoked that blanket benefit and demanded receipts.

The implicit checklist for any future capex announcement now reads:

- Is there an external customer for the compute? (Cloud > Internal R&D)

- Is there a contracted backlog growing as fast or faster than capex?

- Is the operating margin of that customer-facing line expanding?

Alphabet checks all three. Microsoft checks one and a half. Meta checks none. The dispersion in tape reactions is precisely calibrated to that scoring.

Why Korean Memory Doesn’t Read META -9% as a Short

This dispersion does not translate into a bearish signal for HBM names. The total addressable demand for high-bandwidth memory is set by the sum of hyperscaler capex, not by any single name. With Alphabet adding $5-10B at the top end and Microsoft and Amazon also increasing, total hyperscaler spend in 2026 still sets fresh records.

SK Hynix holds roughly 57% global HBM share. Samsung holds roughly 22%. Together, that’s nearly 80% of supply for the dominant memory category in AI training systems. As long as the aggregate capex line trends up, pricing power for HBM3E into HBM4 transitions stays favorable.

Trading rule: don’t read META -9% as an HBM short. Read the four-name capex aggregate. It is up.

My Verdict and Positioning

Overweight: Alphabet (GOOGL). Cloud backlog growth ($460B+, ~2x QoQ) is the cleanest piece of forward visibility in megacap tech. The capex justifies itself.

Overweight: Korean memory (SK Hynix, Samsung Electronics) via direct or KOSPI semis exposure. Aggregate hyperscaler capex is rising regardless of the GOOGL/META dispersion. HBM share is concentrated. Pricing risk is asymmetric upward into HBM4.

Watch: Meta (META). The thesis isn’t broken — better ad models can drive ARPU. But the market needs a Q2 print showing ad revenue growth re-accelerating to absorb the capex burn. Until then, position size should reflect that the burden of proof has shifted.

Trim: Microsoft (MSFT). Not bearish, but the relative growth signal versus Alphabet is now negative. If Azure can’t reaccelerate above 30% in Q2, the multiple compresses further. There are better risk/reward setups in the same sector.

Avoid as a sector trade: Don’t try to short the AI capex theme broadly. The Alphabet print confirms that monetization is real where the channel exists. The trade is dispersion, not direction.

Disclosure: This is analysis based on public filings and market data. Not investment advice. Position accordingly to your own risk tolerance and time horizon.