TL;DR

- Historic Split: Powell’s final FOMC produced 4 dissents — the most since 1992 — with doves and hawks pulling in opposite directions.

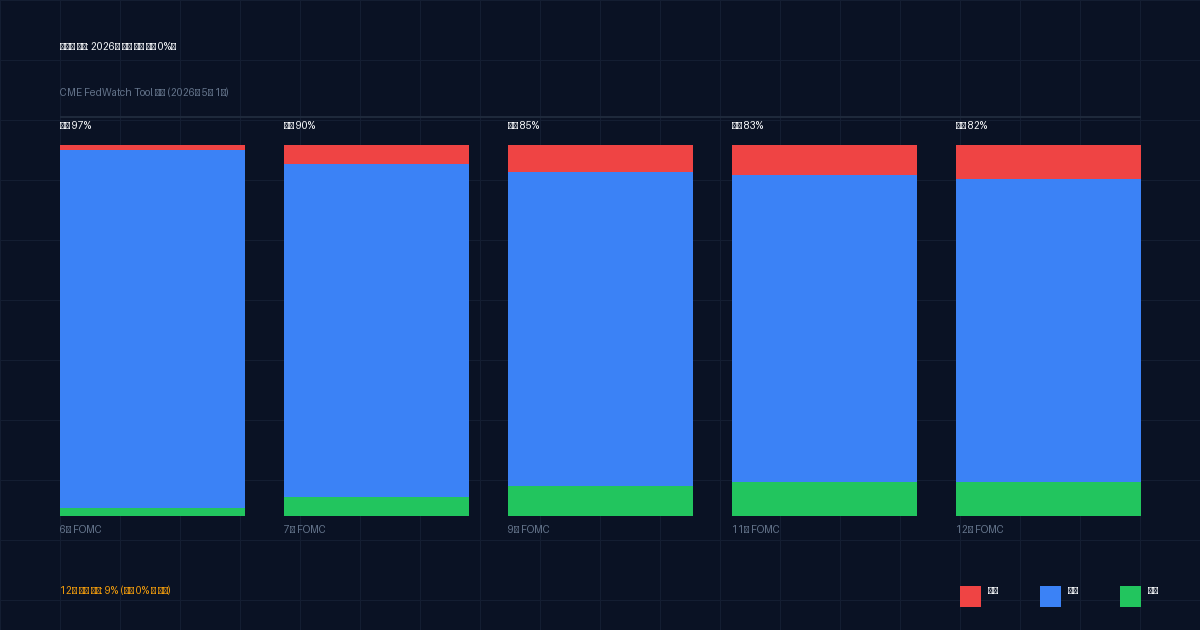

- Zero Cuts in 2026: CME FedWatch now prices effectively 0% chance of a June cut, and markets are even starting to price in a December hike at 9.1%.

- Warsh Era Begins May 15: A known hawk takes the chair. Uncertainty about Fed independence from White House pressure defines the next chapter.

The Numbers That Matter

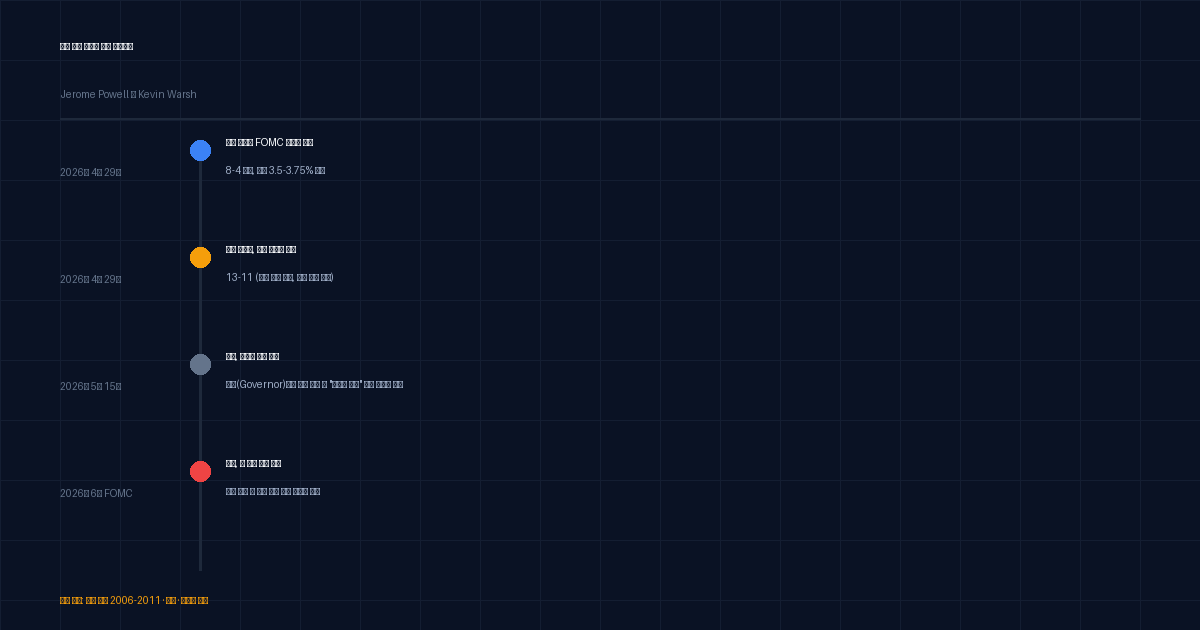

The April 29 FOMC decision, on the surface, was unremarkable: rates held at 3.5–3.75% for the third consecutive meeting. The real story lives in the vote count.

8-4. That is the split. Four FOMC members dissented, the most since September 1992 — over three decades ago. The split wasn’t random noise. It reflected a genuine schism in the committee’s view of where rates should go next.

Key data points:

| Metric | Value | Context |

|---|---|---|

| Fed Funds Rate | 3.5–3.75% | Unchanged, third straight hold |

| FOMC Dissents | 4 | Most since 1992 (34 years) |

| June Cut Probability | ~0% | CME FedWatch as of May 1 |

| 2026 Any-Cut Probability | <10% | Down from >30% in January |

| December Hike Probability | 9.1% | Was 0% the prior day |

| S&P 500 Under Powell | +12.9% avg/year | 2018–2026 benchmark |

What Actually Broke at This Meeting

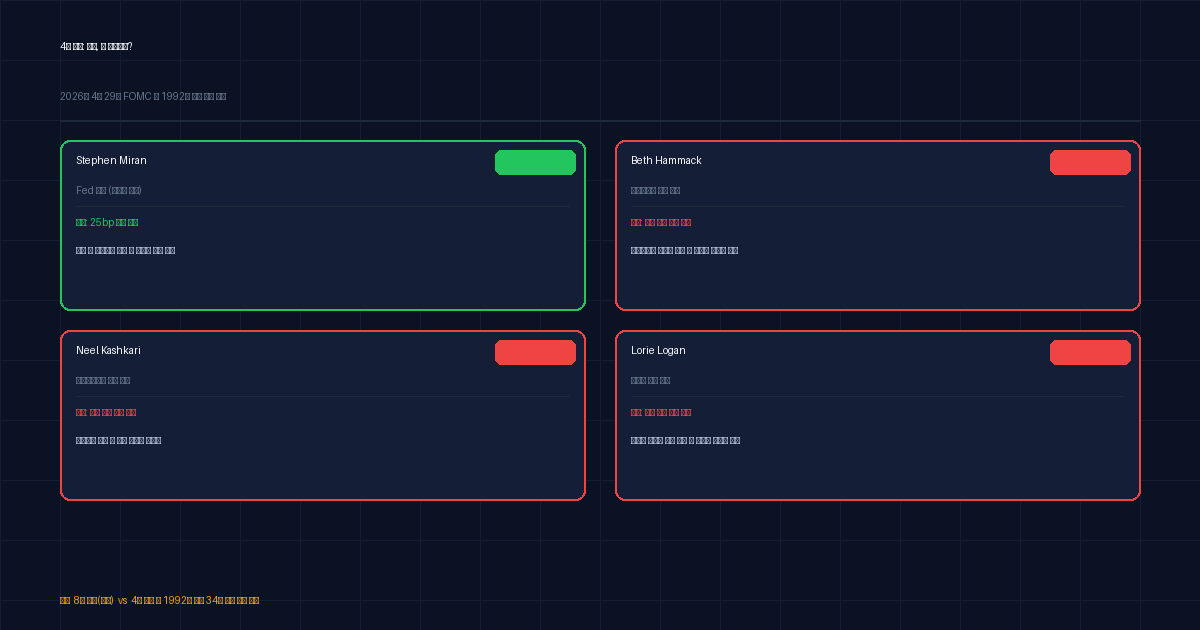

The 4 dissents were not a unified bloc — they came from two irreconcilable directions.

The Dove: Stephen Miran, a Trump appointee, voted to cut by 25 basis points. His argument: tariff-driven stagflation risk — rising consumer prices plus slowing growth — argues for preemptive easing.

The Three Hawks: Beth Hammack (Cleveland), Neel Kashkari (Minneapolis), and Lorie Logan (Dallas) all voted against the statement’s easing bias. They don’t want a cut; they want the Fed to drop even the implication that one might come. Logan’s worry: resurgent global energy prices reopening the inflation wound.

This is not a FOMC that’s one bad jobs number from a pivot. It’s a FOMC where one faction wants to cut and another wants to potentially hike. The middle eight held, but the center of gravity is ambiguous — and that ambiguity is itself a market event.

Powell Out, Warsh In: Why the Handoff Matters

Jerome Powell’s term as chair ends May 15, 2026. He will remain on the Fed’s Board of Governors — but pledged he will not act as a “shadow chairman.” His record: the S&P 500 compounded at 12.9% annually under his tenure, through a pandemic, zero rates, the fastest hike cycle in 40 years, and a soft landing that few thought possible.

Kevin Warsh enters a different environment.

Warsh served on the Fed board 2006–2011. During the 2008 crisis, he was the Fed’s liaison to Wall Street. In the years after, he repeatedly argued that the Bernanke-era QE was excessive. His Senate Banking Committee vote was 13–11, strictly along party lines. That is a thin mandate.

The critical question: will Warsh be a pure hawk, or will he bend to White House pressure? Trump has explicitly called for rate cuts on multiple occasions. The tension between a hawkish chair and an interventionist president is not a theoretical risk — it is the base case for the next 18 months.

Market Pricing Tells the Real Story

The bond market has absorbed this transition quickly.

June cut odds: effectively zero. Full-year cut odds: below 10%. The December hike probability moved from zero to 9.1% in a single session. That last number deserves weight: traders are now paying a premium to hedge against the scenario in which the Warsh Fed tightens rather than eases.

The equity market’s reaction has been muted — a reflection of the fact that “higher for longer” is already partially priced in after the January rate expectations reset. What is not priced in is policy incoherence: a Fed chair who can’t credibly commit to a multi-meeting path because political pressure introduces noise into every statement.

My Verdict: Cautious on Rate-Sensitive Longs

Positioning: Reducing duration and growth-multiple exposure until Warsh establishes a clear signal.

The investment thesis here isn’t complicated. Three forces are converging:

-

Zero cut probability in 2026 means the discount rate stays elevated. High-P/E tech and growth names continue to face valuation headwinds that don’t resolve on their own.

-

Leadership uncertainty introduces a policy risk premium that the market hasn’t fully priced. Warsh’s first few press conferences will be closely parsed. Any sign of capitulation to White House pressure could spike inflation expectations and force a rethink of long-duration bets.

-

Hike tail risk at 9.1% is non-trivial. If energy prices spike or tariff pass-through proves stickier than expected, the next move could be up, not down. This is a regime where both directions carry real probability.

What I am watching:

- Warsh’s first FOMC statement language (June 2026) — whether he drops the easing bias entirely signals the hawkish pivot is real

- Core PCE trajectory — if it re-accelerates above 3.0%, the hike scenario becomes consensus

- USD/KRW and 10-year Treasury yield — the cleanest real-time signals of where rate expectations are heading

Tactical moves:

- Trimming TQQQ and long-duration tech exposure

- Rotating toward value, energy, and financials (which benefit from steeper yield curves)

- Holding short-term Treasuries (3–6 month) rather than extending duration into this uncertainty

Actionable Takeaway

The Fed isn’t cutting this year. The chair is changing. The committee is split. For most long-only equity portfolios built on the assumption of a 2026 rate-cut tailwind, this meeting is a signal to revisit that assumption. The S&P 500’s 12.9% annual return under Powell was built on a foundation of predictable, data-driven monetary policy. That predictability is now in question.

Reassess your rate sensitivity. Trim where needed. The June FOMC will be the first real test of what the Warsh era means.

Investment Disclaimer: This article is for informational purposes only and does not constitute investment advice or a recommendation to buy or sell any security. All investment decisions and their outcomes are solely the responsibility of the individual investor.

Sources: CNBC, Al Jazeera, Axios, Yahoo Finance, Federal Reserve Press Release (April 29, 2026), CME FedWatch Tool, CBS News